The Child Tax Credit has undergone several changes over the years. The mechanics around refundability, phase-outs, and advance payments matter most when you're navigating MAGI thresholds — and that's where intentional tax planning can preserve real dollars per child.

Overview of recent changes

Notable structural changes to the credit have included:

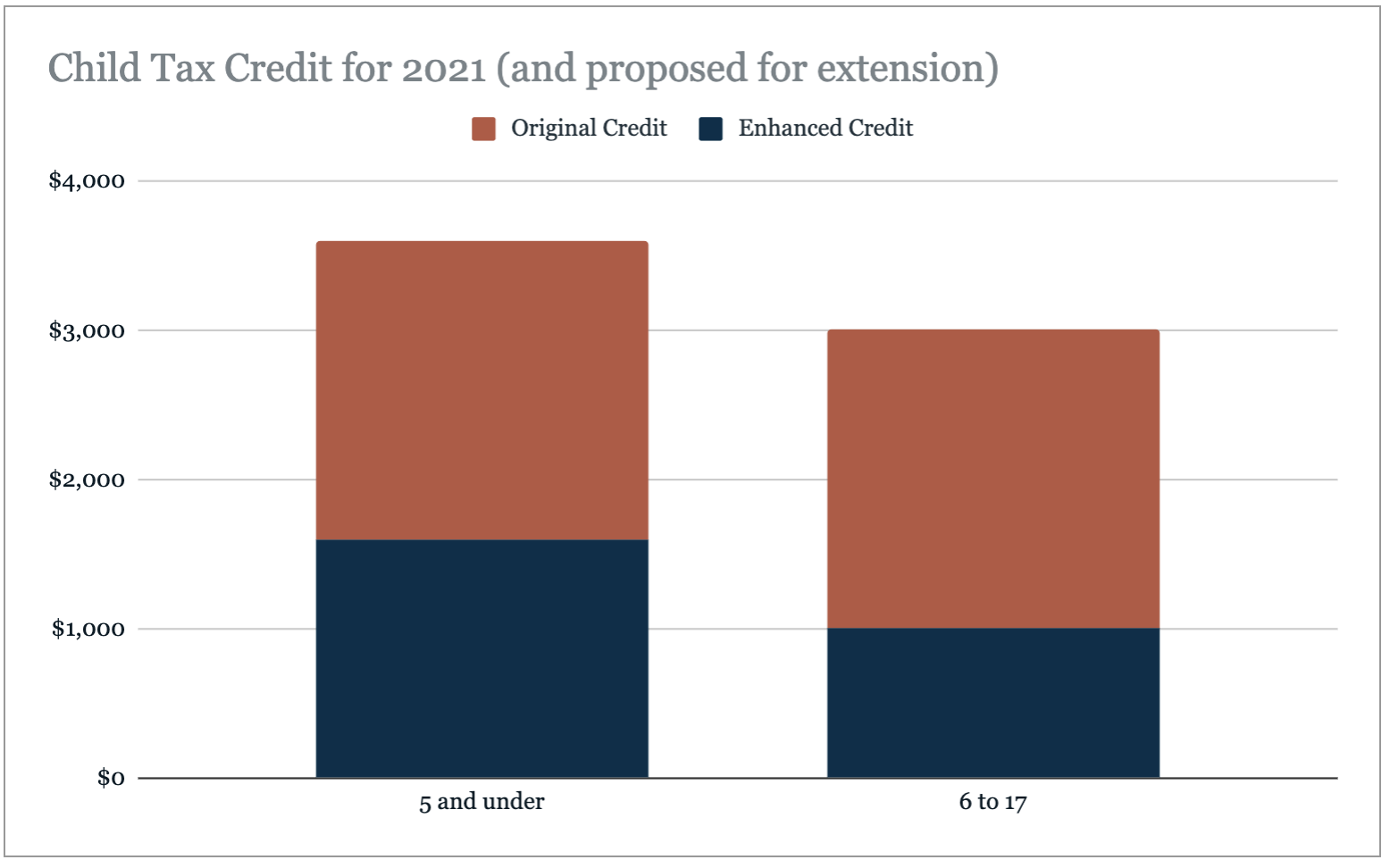

- Increased per-child amounts (with higher amounts for younger children).

- Removal — and at times reinstatement — of an earned-income requirement.

- Shifts between fully refundable and partially refundable.

- Advance monthly payments instead of a year-end credit.

- A two-step phase-out based on modified adjusted gross income (MAGI).

Tax credits are either refundable or nonrefundable. A refundable credit can take liability below zero, creating a refund. A nonrefundable credit cannot. Refundable credits are much more attractive to the taxpayer and ensure that everyone within the income range gets the entire credit. When there is a nonrefundable element, we essentially create both a floor and a ceiling — which is why expansions of CTC have historically helped middle-income taxpayers more than lower-income ones in some configurations.

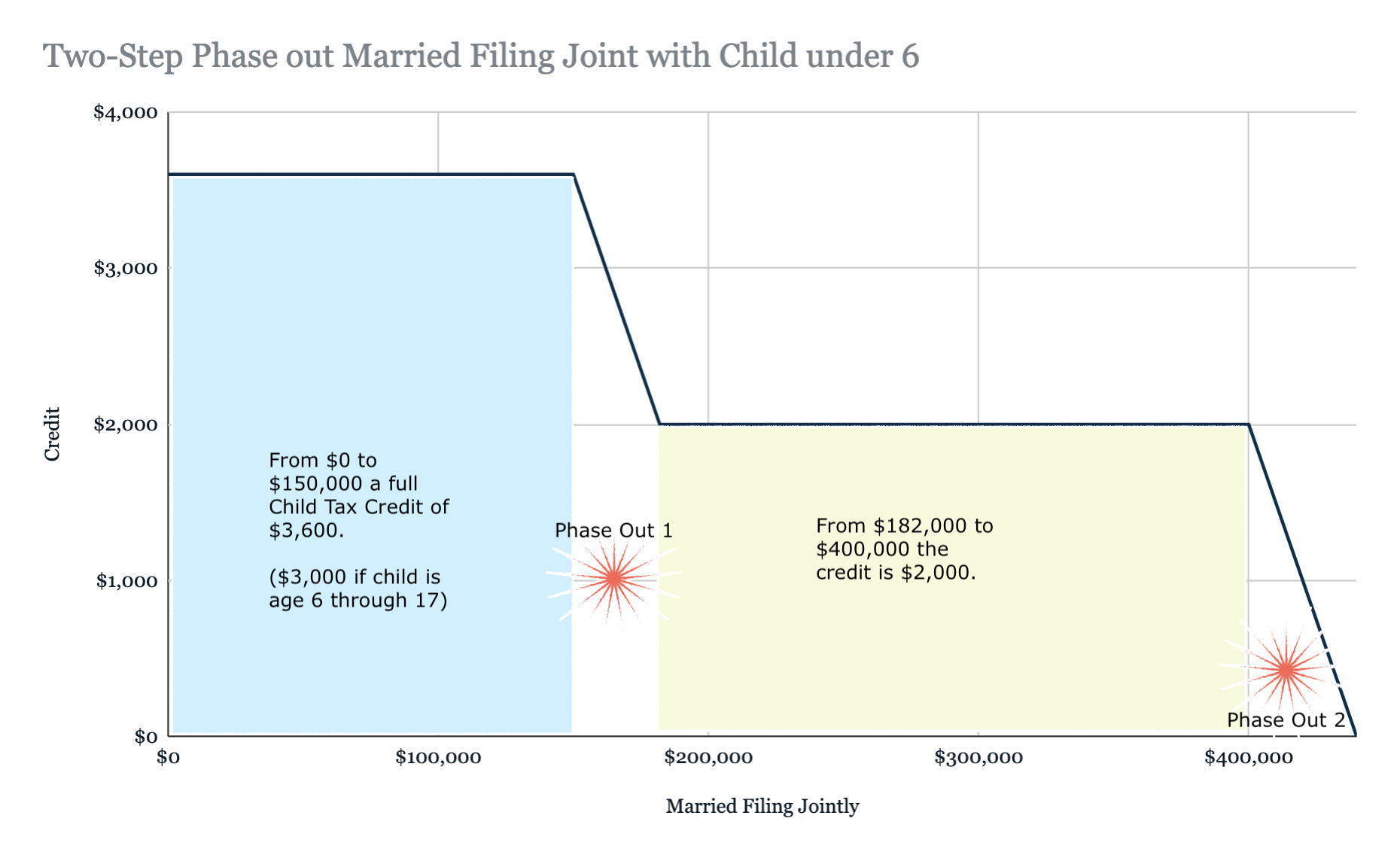

The two-step phase-out process

When in a phase-out stage, the credit is lowered by $50 for every $1,000 of income in excess of the income limit. It's two-step because it starts in Phase 1 and then stops until the taxpayer reaches Phase 2. Phase 1 typically only impacts the "enhanced" portion (the amount above the base credit). The chart below shows the two phases for MFJ.

The timebomb from advance payments

When the credit is sent monthly to taxpayers, the tax return won't have a credit applied at filing. I've seen examples where a self-employed parent might generate a tax liability of $6,000 prior to using the CTC, but owe $0 due to having three children. That person may pay no estimated tax during the year while also receiving $9,000 in advance credits. When filing, they have paid $0 and still owe $6,000 — possibly with penalties and interest attached.

If you're in this situation and have access to payroll, using withholding is a better way to catch up tax payments later in the year, because withholding is always considered paid on January 1st, whereas estimated tax is considered paid when remitted (i.e., it would be late).

Payroll remitted is always timely paid. Use it to catch up by adding additional withholding.

Tax planning with the CTC

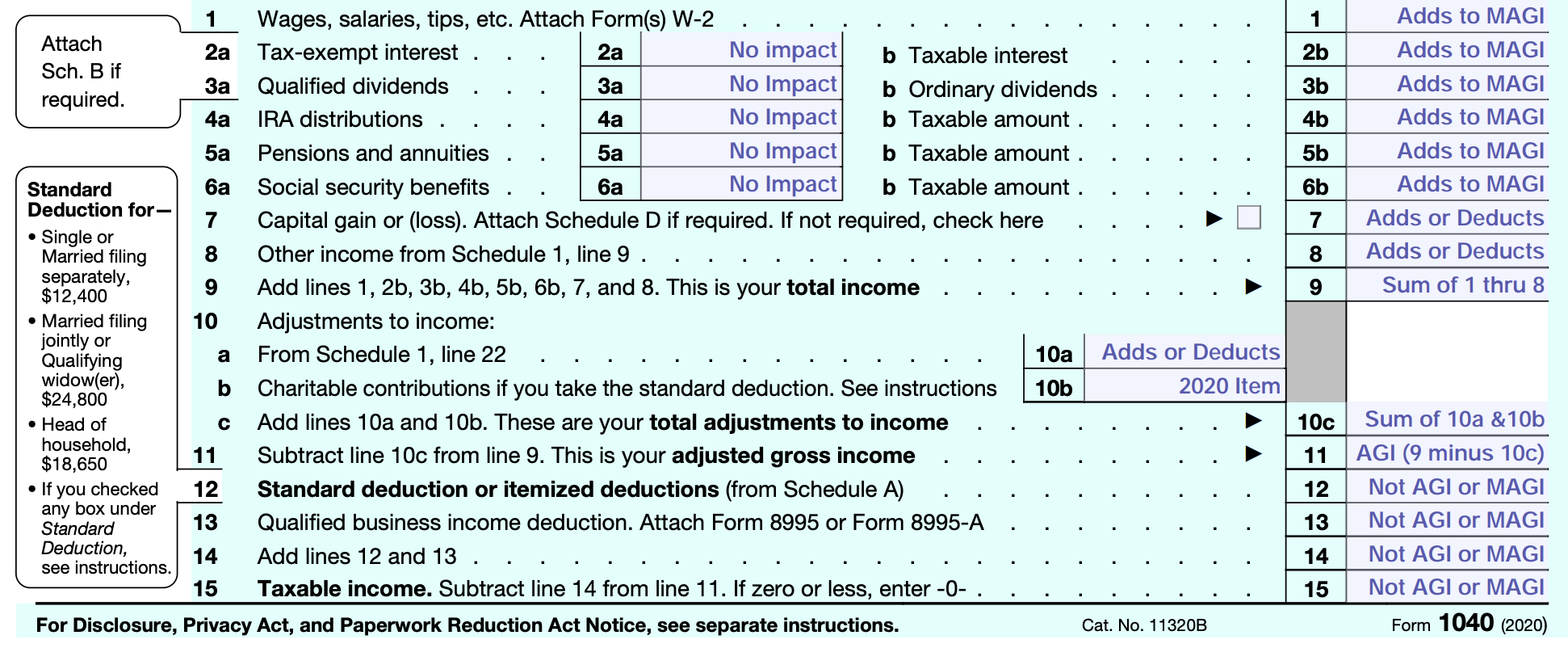

Managing your MAGI is the lever. Most filers use Line 11 of the 1040 for MAGI (the AGI). The "M" in MAGI is the modification made to Line 11, which differs based on the credit in question. For the CTC, the modifier is foreign earned income (including PR and American Samoa).

CTC planning is limited in scope to cases where you're near one of the two phase-out steps. A taxpayer with MFJ income of $300,000 isn't going to pull themselves back into a credit much above the base, but a taxpayer on target for a MAGI of $184,000 could find benefit. There are two strategies: lower the additive items, and raise the deductive items.

Lines we can impact on the 1040

- Line 1 Wages — lower via paycheck pretax items (401(k), HSA, medical, etc.).

- Line 2b Interest — use a mortgage as a tax-deferral tool, or gift down to children.

- Line 3b Dividends — tax location (avoid dividend stocks in taxable accounts), gifting down if appreciated.

- Line 4b IRA distributions — avoid pretax conversions unless intentionally increasing income.

- Line 5a Pensions and annuities — avoid annuities.

- Line 6b Social Security — delay for enhanced future benefits and use interim years to control MAGI.

- Line 7 Capital gains — loss harvesting up to $3,000 can be a negative line item for MAGI.

Many wage earners think they don't have many options, but there can be lots of planning opportunities providing the broader financial picture is well constructed. For example, it is very common to have a person with a low-rate mortgage they're paying interest on (which is rarely fully deductible), who is also earning taxable interest at near-zero rates. If they instead sweep cash into the mortgage, it becomes an insulated wrapper for MAGI purposes (similar to the annual benefits from a 401(k)) and eliminates the Line 2b impact.

Appropriate gifting of assets to children (within gift-tax and kiddie-tax guardrails) can also be an effective strategy to lower these income levels.

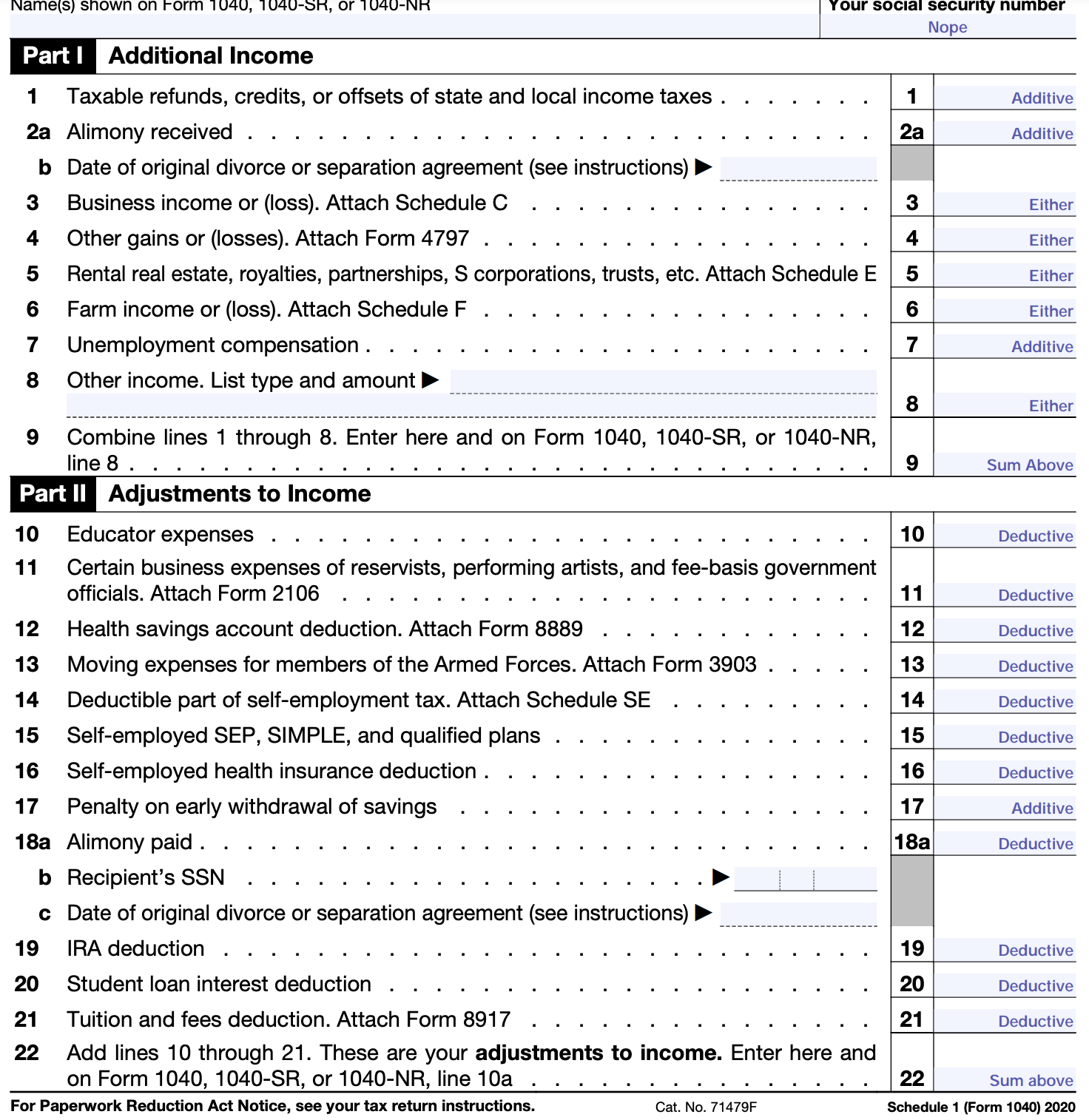

Schedule 1 clues

The 1040 sends us to Schedule 1 for further planning opportunities.

Strategies on Schedule 1

- If you didn't max out your HSA via payroll (the superior method due to FICA exemption), you can top it up manually until 4/15.

- Traditional IRA deduction can be made until 4/15. The primary taxpayer may be over the income threshold, but a non-working spouse may have a Spousal IRA option that's frequently overlooked.

- If you had a business that lost money, you can deduct it.

- If you had a business that made money, you can deduct health insurance and retirement plans here.

- Rental losses are deductible up to $25,000 when AGI is under $100,000 — Schedule 1 deductions can combine and cascade.

- Taking the tuition and fees deduction instead of the American Opportunity Tax Credit would lower MAGI — but at the cost of a more attractive credit, so it needs careful modeling.

- W-2G recipients can use session-based netting to calculate net win/loss via Schedule 1 rather than relying on Schedule A, keeping MAGI low. Retirees use this to reduce taxation of Social Security benefits — MAGI is used in many places beyond the CTC.

Many of these are tweaks and adjustments, but combined they can fine-tune MAGI and increase credits. It's important to run multiple scenarios — sometimes it's beneficial to move MAGI upwards instead of downwards to capture the best benefit overall.

Swapping government cash for appreciated assets

A fun example of planning: an employee of a utility company who participates in an Employee Stock Purchase Plan (ESPP). Often such employees hold the stock long-term and it has appreciated. This creates a quandary:

- Should I sell, and create a capital gain?

- Should I hold, and receive a dividend (utilities tend to pay high dividends)?

The best plan is always to sell ESPP on the day of grant, but some companies enforce a holding period of up to 12 months, meaning this question arises annually.

If the stock is valued at $100,000 with $3,000 of capital gains and a 3% dividend, the choice to hold vs. sell is roughly equal for current-year MAGI. If the individual is at $182,000 MAGI excluding this stock, then each $1,000 of gain or dividend would cost $50 of lost CTC — per child.

Solution: gift, then kiddie-tax rules

The taxpayer could gift $30,000 (married, splitting) to each child. With 4 children, split-gifting $25,000 to each completely moves the $100,000 out of the parents' 1040. The $3,000 of MAGI saved results in $600 ($150 × 4) increase to the CTC.

Kiddie tax occurs with unearned income to the child above the annual threshold.

When kiddie tax occurs, the child must either file (and pay) tax on their own 1040 at their parents' tax rate, or the parent can report it on their 1040 to avoid the filing requirement.

Interestingly for CTC planning, we could argue we don't care about kiddie tax — even if we are subject to paying it, we moved it away from MAGI on the parents' return and reported it on the child's 1040. This doesn't avoid the tax due on any excess, but it does allow us to capture the CTC.

Note: with kiddie tax, all children sum to a single threshold. If the children hold the stock and receive dividends, they may trigger kiddie tax. Dividends are often paid quarterly, so it's possible that if you gifted in Q3, you could have the children realize the threshold amount in capital gains by selling in the current year, wait until January 1st to sell the remaining stock, and even with an interim ex-date, the sum could stay below the next year's kiddie-tax limit.

The final piece would be to push cash that was cleaned of unrealized gain back out of the child account and into something further tax-advantaged — a 529, or additional mortgage payments. This requires coordination with other factors such as dependent support tests.

End result: increased credits captured, appreciated assets liquidated at no (or low) cost, and added diversification away from employer risk.