Series I Bonds are issued by the US Treasury. They have characteristics that make them attractive in times of high inflation. With the right setup, a household can stretch the $10,000 per-SSN limit, capture education benefits, and use kiddie-tax mechanics to earn interest at a 0% effective tax rate.

Pros and cons

| Pros | Cons |

|---|---|

| Low risk (US government bonds) | Illiquid (cannot sell for first 12 months) |

| High return when inflation is elevated | Interest is variable, resets every 6 months |

| State tax-free always; sometimes Federal tax-free | Clunky purchase site; paper bonds may be lost |

| Education benefits subject to AGI limits | Harder to integrate with a holistic portfolio |

| Kiddie-tax / low-income benefits via accrual election | Requires good record-keeping for tax recognition |

Characteristics of the bond

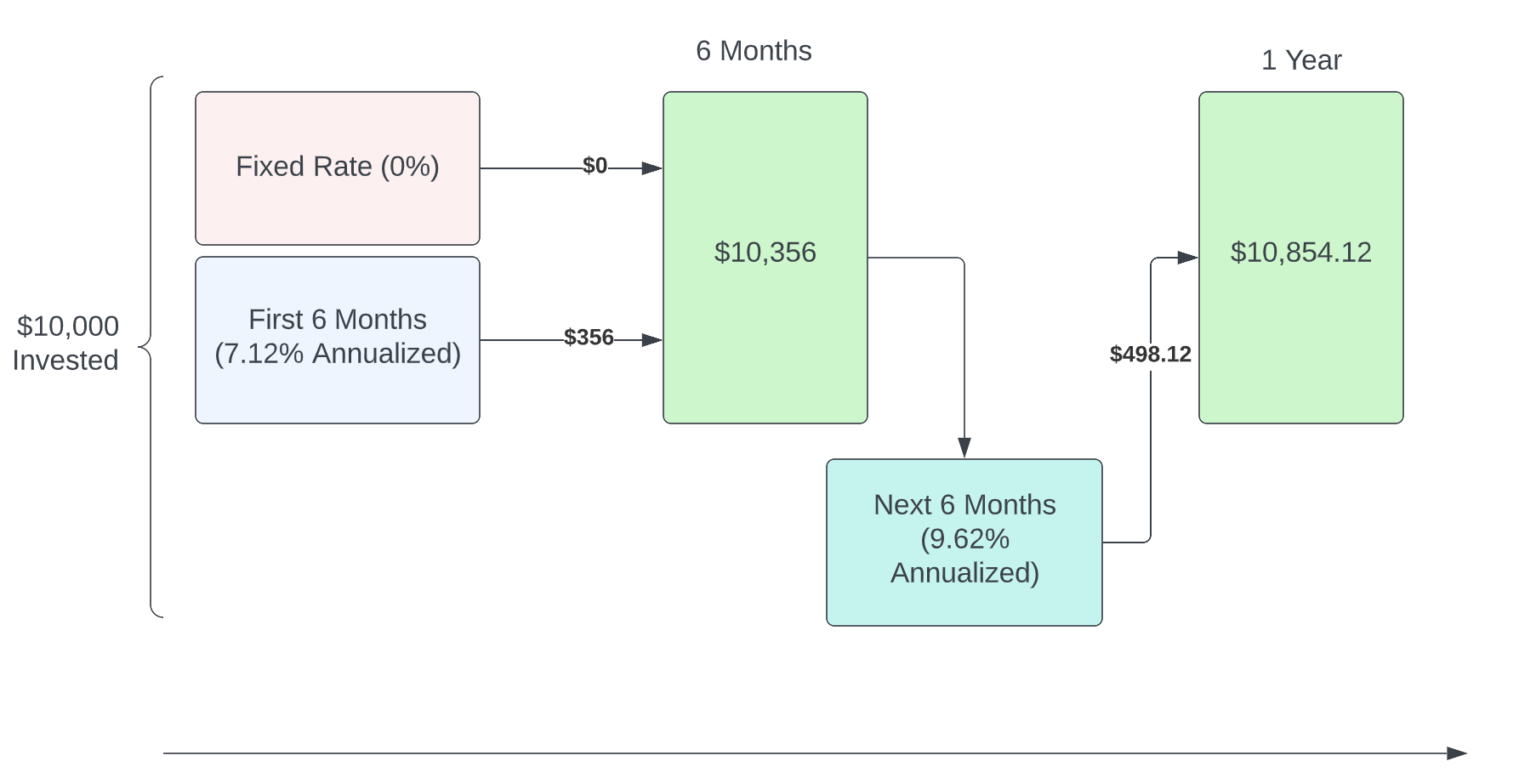

Series I Bonds are sold at face value and accrue interest monthly for 30 years, or until sold (if sooner). They have two components of interest:

- Fixed Rate: remains constant for the lifetime of the bond.

- Variable Rate: resets semi-annually based on inflation. Interest accrues monthly but compounds semi-annually.

The two rate types combine to form a Composite Rate, with three components: the fixed rate, the first 6-month variable rate, and the second 6-month variable rate.

Power of compounding

For the first 6 months an initial $10,000 investment earns interest at the first variable rate. At the 6-month mark, the rolled-up balance starts earning at the new rate. Note that if you buy in April you'll earn the April rate for the first 6 months and the May rate for the next 6; if you buy in May you get the May rate for 6 months and "whatever the rate is in November" after that.

Strategies to maximize value

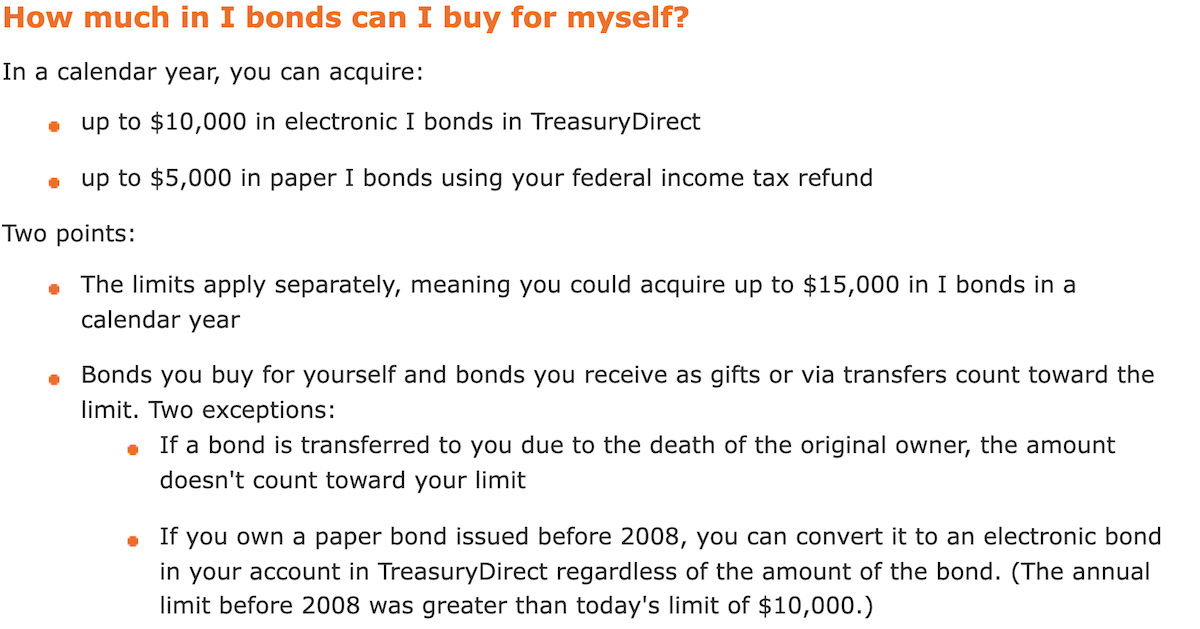

The initial strategy is to apply for the maximum amount of Series I Bonds: $10,000 per SSN, plus $5,000 from your tax return. Here are some ideas to stretch the concept further.

Superfunding — how far can you push the limits?

The greatest restriction on purchasing Series I Bonds is not the per-SSN cap; it's your own approach to risk and ethics. Ethical questions are best solved at the individual level, providing the strategy is legally sound.

The limits are set to $10,000 per person plus $5,000 per tax return. There are a couple of exceptions:

- Bonds bought as gifts can be stored in a "gift box." This allows you to store multiple purchases (but may require retitling later if linked to different SSNs). You may hold a bond in the gift box for up to 30 years.

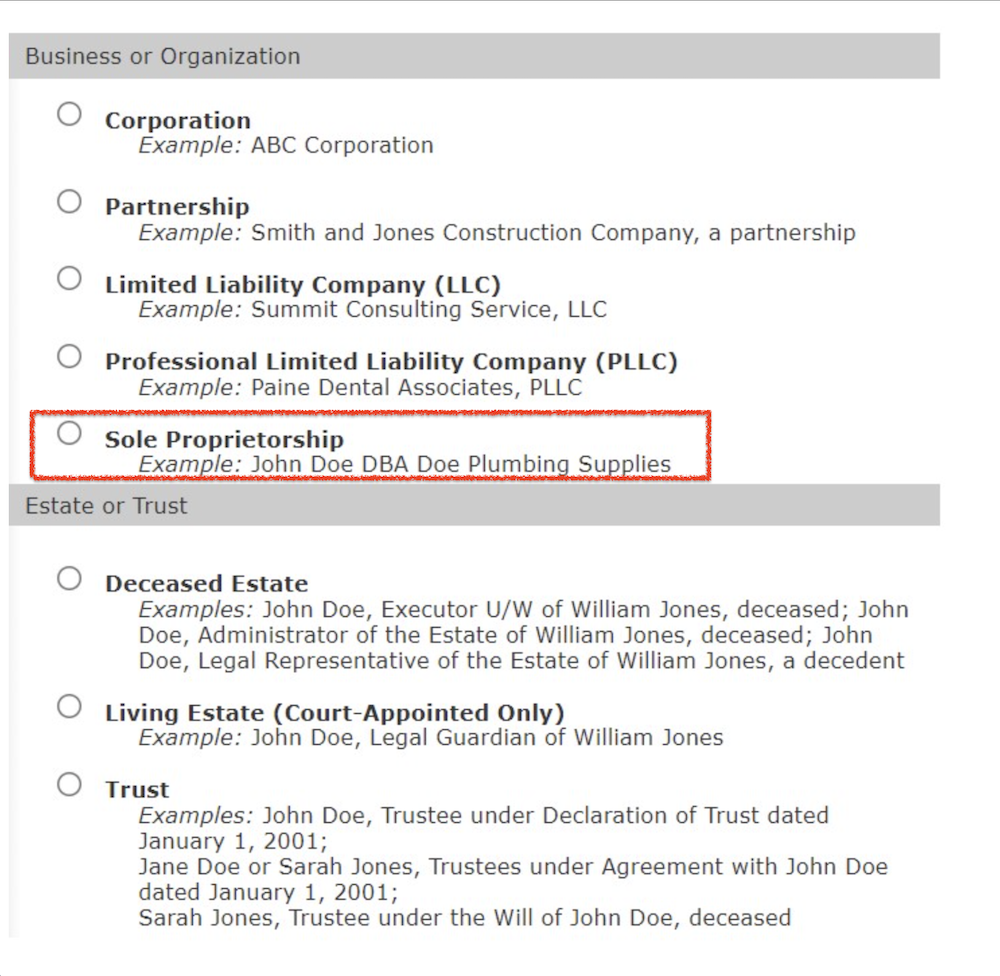

- Bonds may be bought by businesses and trusts. This allows a person who is the owner (or beneficiary) of such an entity to hold more than $10,000.

An unincorporated business with merely a DBA status is eligible to own a bond. Based on how the system tracks ownership, you'd need an EIN for each business or DBA holding bonds.

How much is too much?

I was initially skeptical about using entities to bypass the annual limit, but as a person who owns several legitimate businesses, I can see the value in each holding Series I Bonds to protect purchasing power and help cover inflation-sensitive expenses. The fact that there is an option for an entity as casually designed as a DBA reinforces the notion that a person may buy a bond, and a business may also buy one. Beneficial ownership is arguable — the asset is owned by the entity and may be transferred via the sale of the entity.

Impact on basis

A benefit of the business holding the bond is that the asset remains in the business, impacting basis. If an S Corp owner withdraws $10,000 to buy a bond personally, that's a distribution of capital (an owner's draw). If the business buys it instead, the bond is carried on the balance sheet, affording the same benefits without impacting draw.

To an S Corp owner who can only afford one bond, buying within the business and carrying on the balance sheet is preferable. For someone who can afford more than one, this is a viable approach.

Trust and estate considerations

I have seen people attempt to purchase like this:

- Trust (revocable) for Spouse 1

- Trust (revocable) for Spouse 2

- Personal name Spouse 1

- Personal name Spouse 2

Total: $40,000. Beyond requiring multiple EINs, this conflicts with the approach of holding all assets within a revocable trust. While this can be acceptable with transfer-on-death designations, it does increase the risk of an estate-planning mistake and may reintroduce probate concerns. Since both individual and business ownership can create this complication, factor it in for those seeking more than $10,000 per SSN per year.

Kids: kiddie tax vs. education benefits

One idea is to buy Series I Bonds for everyone with an SSN in the household — parents and children. Two interesting things about kids:

An election may be made to receive the income annually (the default is to receive it on maturity or sale). If you buy in the child's name, a lot of interest may be tax-free. The child may earn a meaningful amount tax-free at the child's standard-deduction level. As standard, the Series I Bond is exempt from State tax (as a Treasury bond), so a majority of growth could be tax-free, depending on how quickly the interest compounds.

It is worth noting that a child who uses a Series I Bond for education in their own name may not claim the education benefits a parent may claim. On the other hand, if the parent owns the bond and redeems it in the same year they incur education costs, they can exclude the interest created on redemption.

Keep in mind AGI limits apply to this parental benefit, so for those in higher income brackets a better strategy might be to leverage the kiddie tax, then have the child liquidate the bonds prior to FAFSA evaluation times.

What if you can't afford it? Debt arbitrage

There's an old adage in the financial industry called the 3-6-3 rule: a banker is happy to borrow at 3%, lend it at 6%, and be on the golf course by 3pm. The key is perceived equal risk in the borrowing and lending — a risk-adjusted profit. Where others make a mistake is when they borrow (mortgage, margin, etc.) to invest in an unequally risked product. You see this when people say they would rather invest in the stock market than pay off their mortgage.

The 401(k) loan example

You may borrow 50% (capped at $50,000) from your 401(k), to be repaid over no longer than 5 years. You must pay interest at a rate around WSJ Prime plus a spread. Removing equity risk from the equation, you'd pay a small interest cost to earn potentially much more in I-Bond interest. Keep in mind: if you lose your job, your loan can be instantly due for repayment, which conflicts with the 12-month I-Bond lockup. A person might also borrow from their 401(k) to fund a child's Series I Bond and pay no tax at the kiddie-tax level.

A replacement for the 529?

Not entirely. A 529 has FAFSA benefits when calculating assets, but I-Bonds can be a complementary component of college savings. Rather than just a 529 we might instead have:

- 529 for 60% of costs

- Series I Bonds (parental owner) for 20% — when AGI limits are favorable

- Series I Bonds (child owner) for 20% — when kiddie-tax rules are favorable

Individual circumstances can influence weighting. While there's a negative aspect to the FAFSA calculation, holding a mix of funds for college reduces concerns about overfunding a plan for a child who might not need a fully funded education (scholarship, etc.).

Helpful IRS forms

- IRS Form 8815 deals with excluding Series I Bonds interest (education benefit).

- IRS Form 8814 deals with kiddie tax (including Series I Bonds).