Series I Bonds drew massive attention when their annualized rate hit 9.62%. Annual purchases are limited to $10,000 per tax ID. After a peak rate, the buy/hold/sell decision becomes less obvious. Here's a framework for thinking through it whenever rates are in flux.

The short answer is usually "buy" when funds permit, but the decision shifts as the rate environment changes. We should always be evaluating the merits of holding them as we get new information.

The difference between not buying and selling

If we consider ultimate conviction in a strategy, you might decide that if you wouldn't buy something, you should short (or sell) it. A caveat: selling newly acquired bonds comes with a loss of 3 months of interest, which could be punitive enough to encourage holding rather than selling. However, a point may come where selling — with penalty — is superior to holding.

Opportunity value

The decision to buy, hold, or sell comes down to a comparison with opportunity value. While the punitive loss of interest might tip the decision toward holding, the scarcity of Series I Bonds (limited to $10,000 per tax ID) can also encourage holding even when slightly less efficient than selling in the short term.

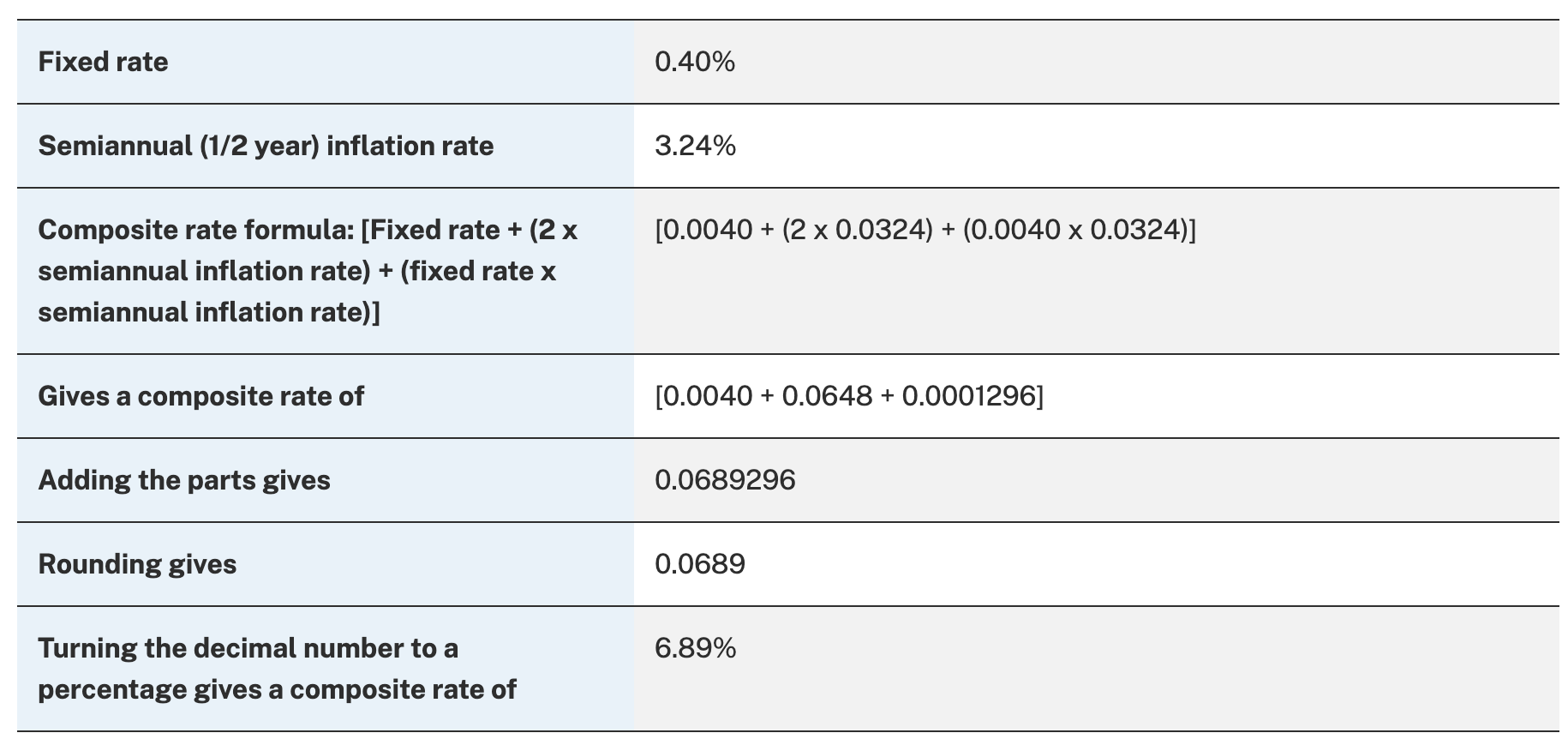

The math

Series I Bonds have two components: a fixed rate set for the entirety of the 30-year bond, and a variable rate that adjusts every 6 months based on CPI-U inflation data. They are Treasury bonds — exempt from state tax and high credit quality. To decide on buying, holding, or selling, we need to compare with a similar-risk investment, which would be another Treasury-issued bond.

Variable interest, guaranteed for 6 months

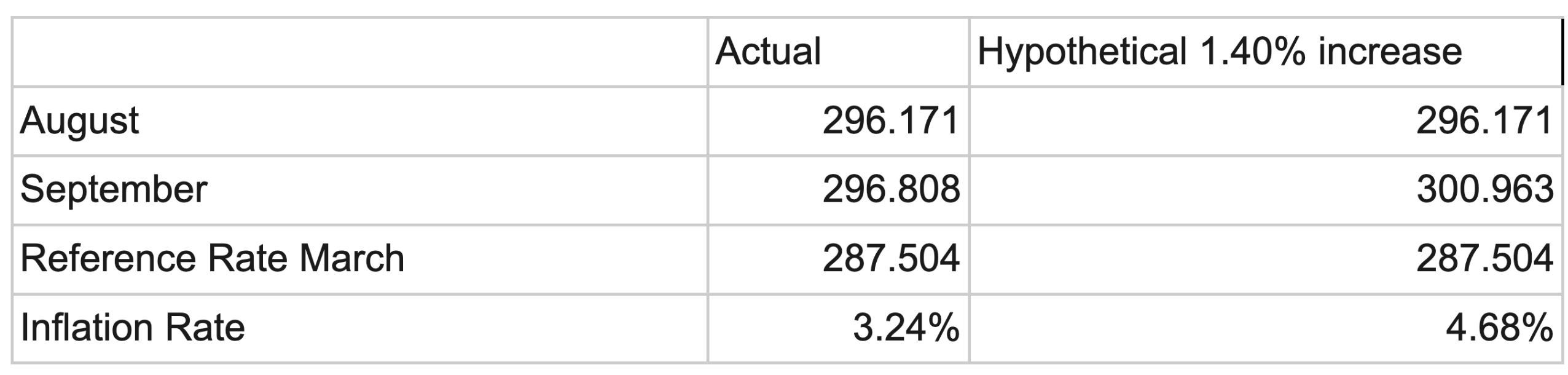

Interest rates are locked in for 6 months. If we wanted certainty on the rate, it's better to wait until just before the inflation reset is announced — May 1st and November 1st each year — since our ability to predict a year of income increases as we get closer to the announcement.

Calculating the next rate — can we see the future?

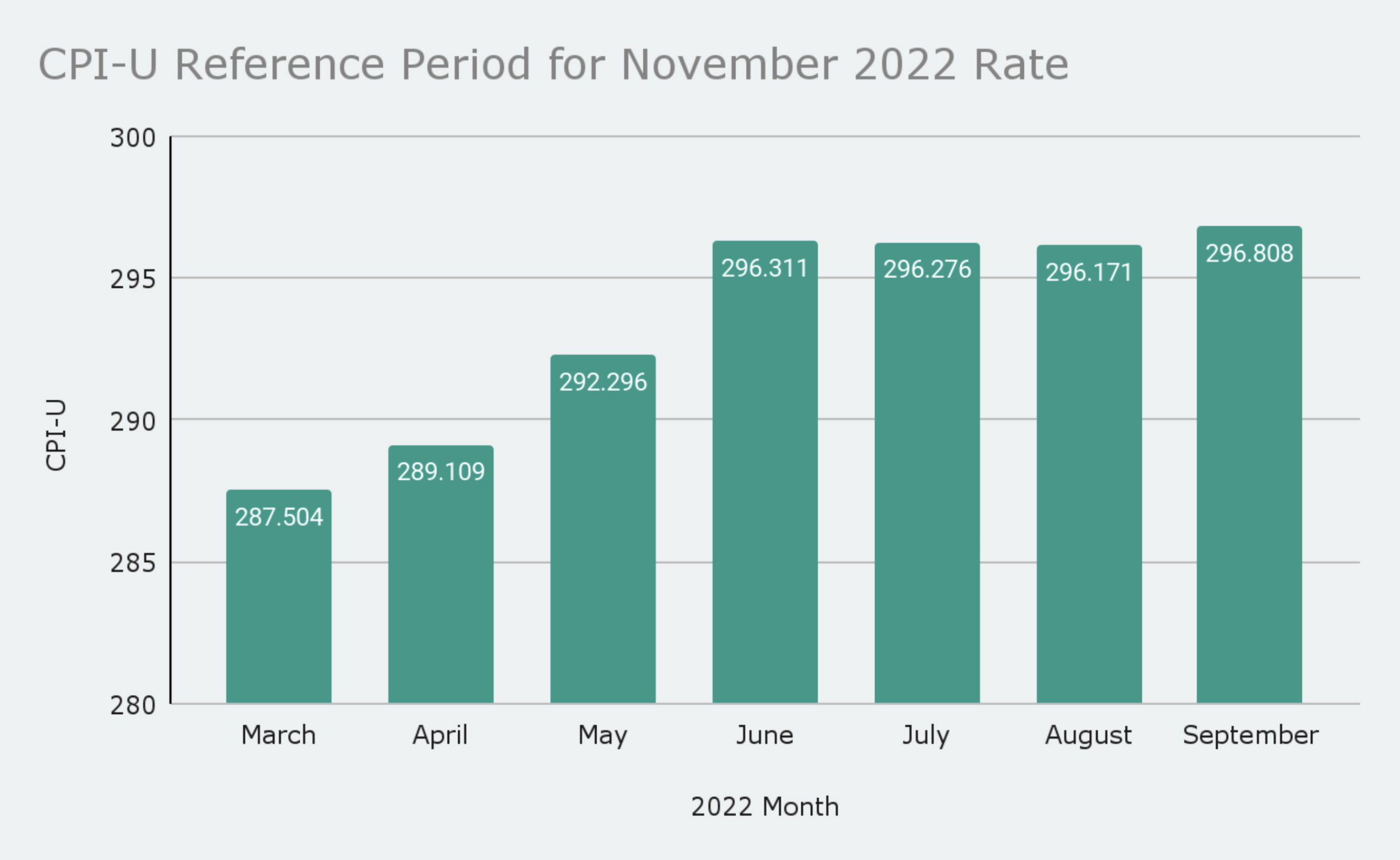

The rate is calculated from CPI-U, publicly available from bls.gov. CPI-U is a trailing 12-month average figure, so mathematically it becomes easier to "box in" a predicted value.

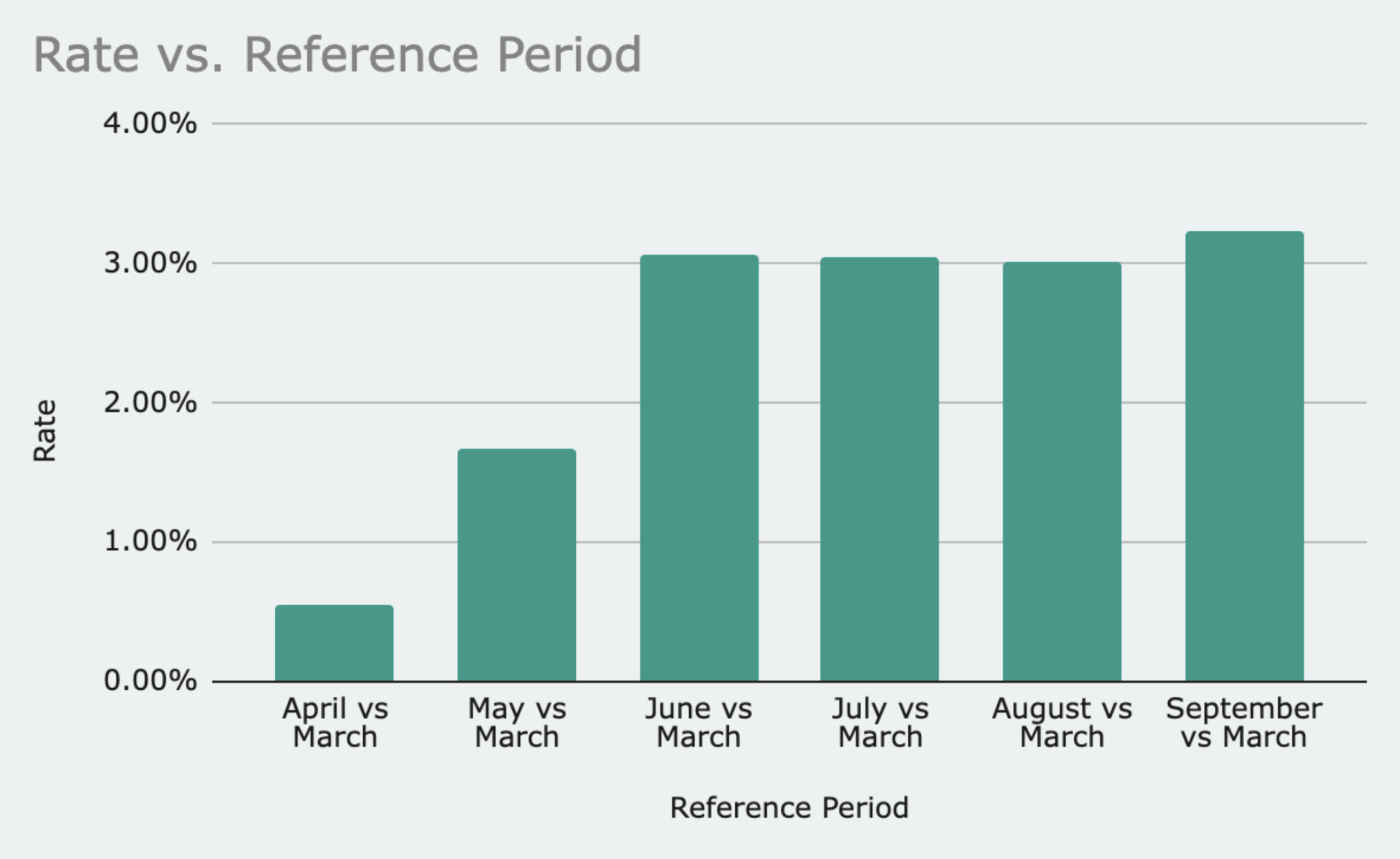

The Treasury Department looks at a 6-month period ending in September to set the November rate, and a 6-month period ending in March to set the May rate. The rate is derived from the percentage change in CPI-U between the two endpoints.

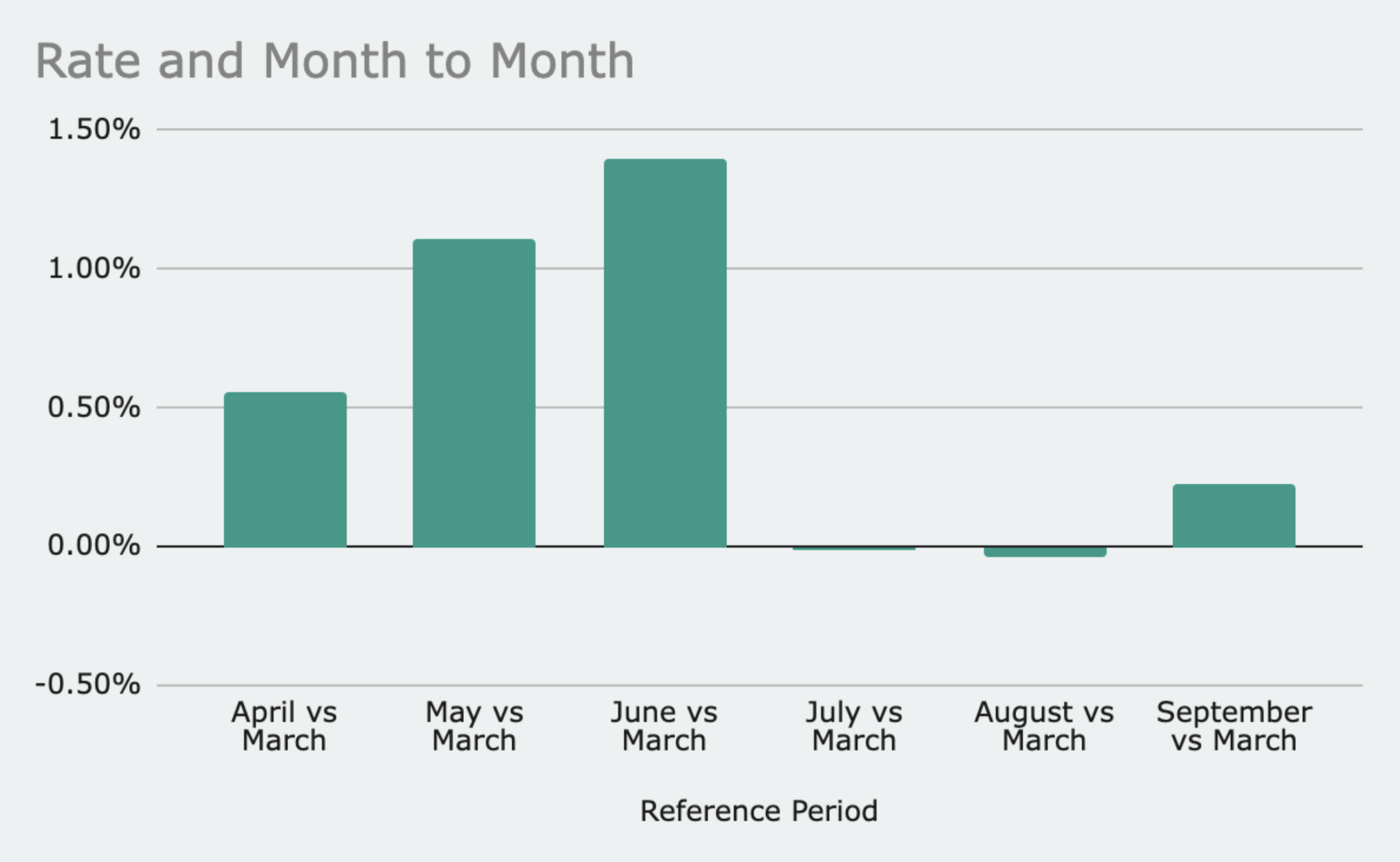

Notice that the rate calculation appears to ignore the months between the two reference endpoints. It simply looks at the percentage change in CPI-U at the two endpoints.

Predicting future rates with unpublished CPI-U

Two paths: fundamental factors that could be quantified (such as mortgage rates), or technical analysis — considering what bounds of probability a number could fall within.

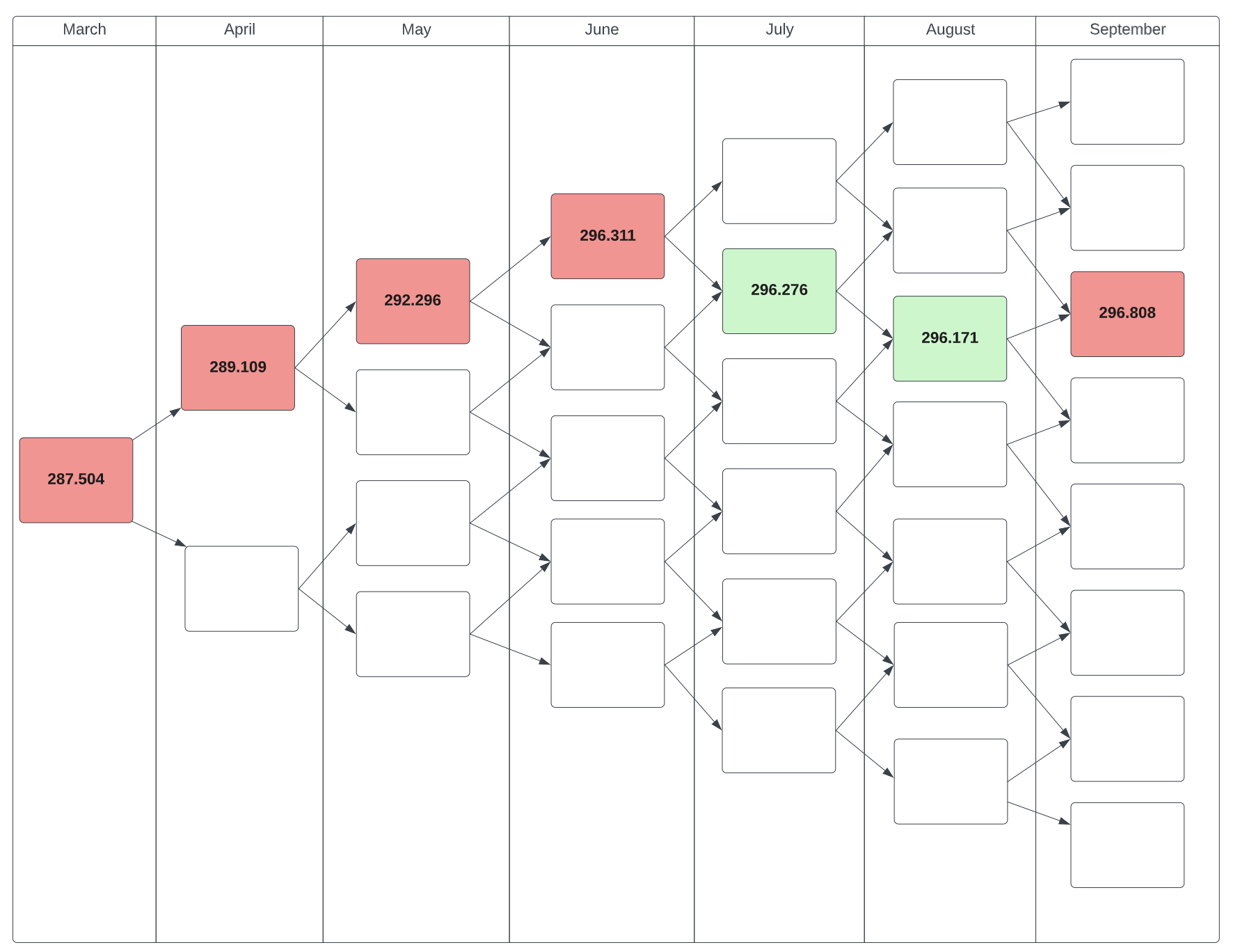

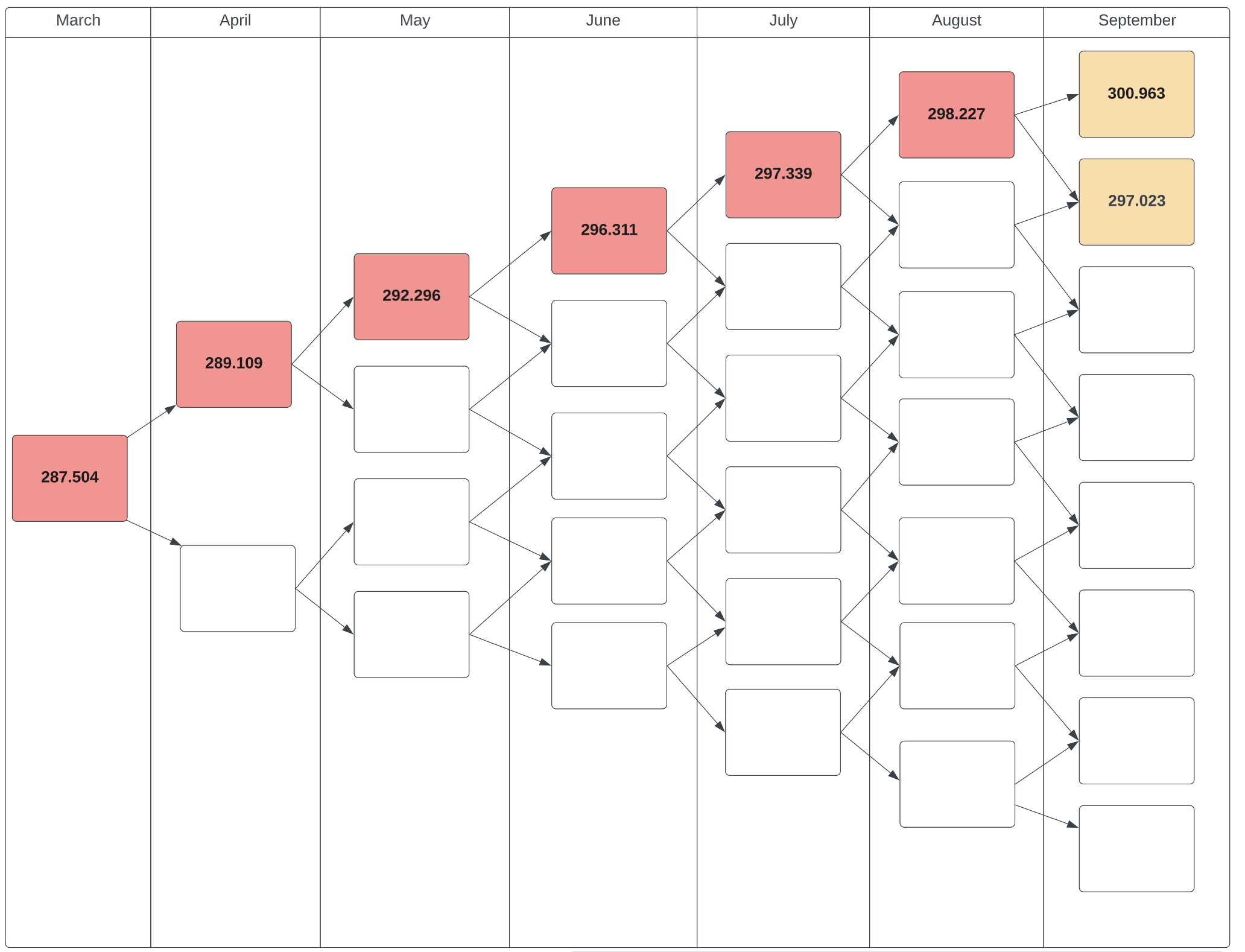

Each month we can move up or down the tree. Predicting a September rate from August seems easier than predicting it from March. Looking at month-by-month changes lets us hone in on an expected range based on the historical average monthly change, considering the probability of movement using standard deviation and a bell curve.

Let the upside go up

With the Series I Bond decision, we're choosing a product that's illiquid for 12 months and loses 3 months of interest if sold within the first 5 years. We're agreeing to be locked into a product with a variable interest rate, one that we might find unattractive as inflation slows. We aren't going into this speculatively in the hope that inflation rises, but rather that it will not fall sufficiently to be an inferior choice.

To examine this, we need to consider an equilibrium price for the bond. If we use the prevailing T-Bill rate as our comparative rate, we need to know what our breakeven price for a Series I Bond would be.

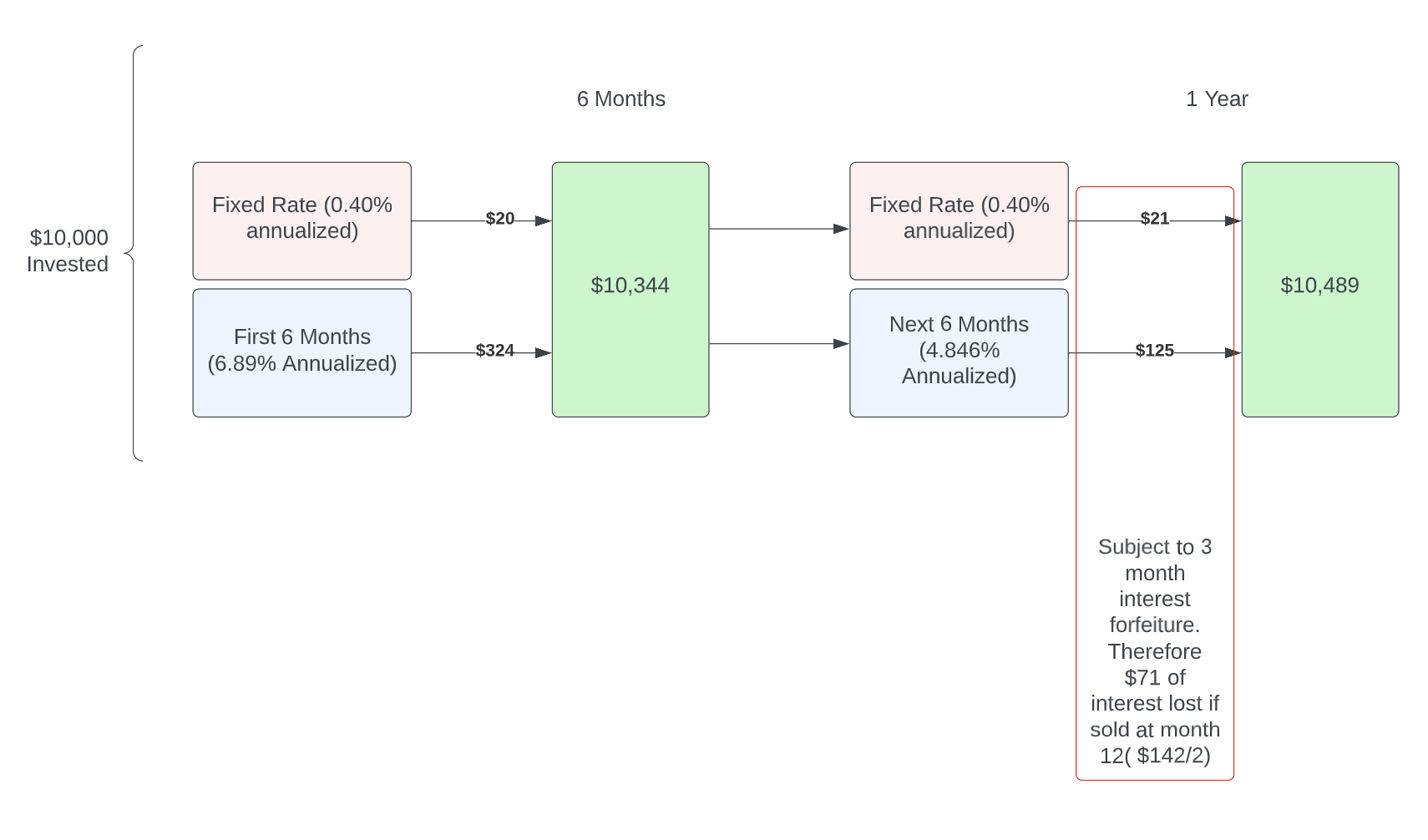

Pricing the penalty

One advantage of the penalty is that it removes the trailing 3 months of interest. Assuming the bond owner has sufficient resources, they should not be selling a bond where losing 3 months of interest is overly detrimental — the reason to sell is that the interest rate has declined to insignificance.

If we have the ability to buy a T-Bill at a comparable yield, we wouldn't acquire a Series I Bond if we knew with certainty it would yield the same — because of the penalty element. But we should also keep in mind the penalty isn't substantial, and if we find an opportunity to exchange the Series I Bond for a T-Bill by incurring the penalty, a calculation at that point in time would allow us to decide.

Timing the sale by knowing what you're earning

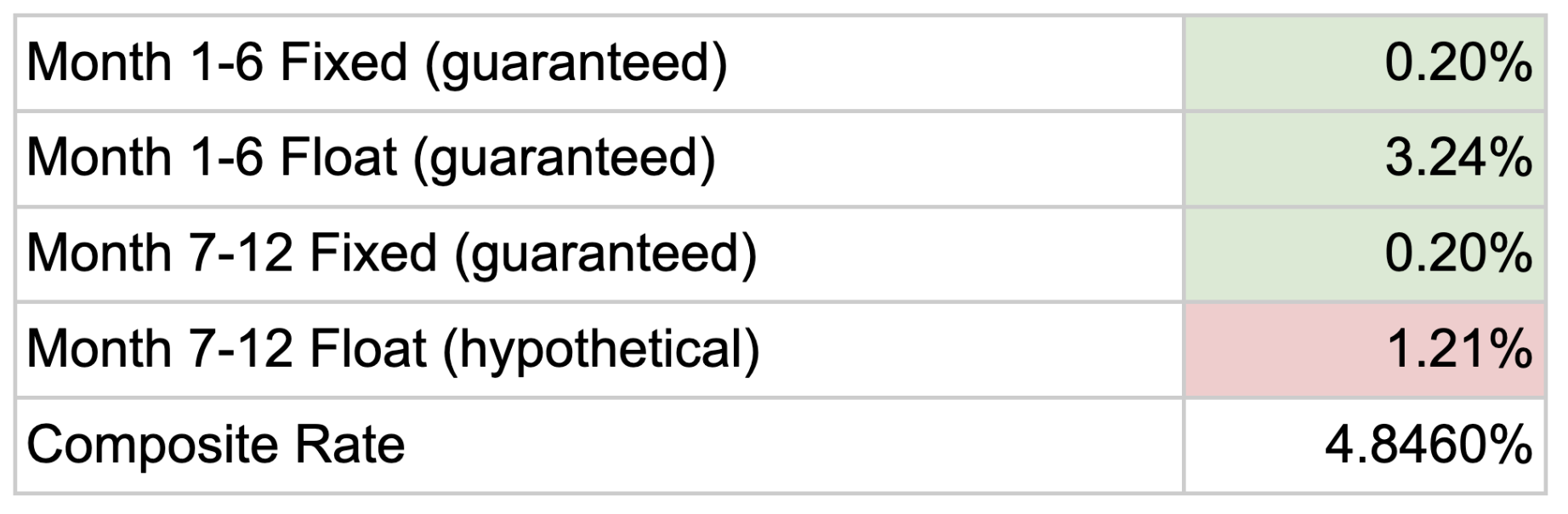

The annualization method of the Series I Bond can be confusing. If we were earning a low rate for the second 6 months, returns would trail the T-Bill rate, and the annualized rate would be carried by the more generous first 6 months. The 12-month lockup prevents us from exiting and forces us to accept the lower rate.

While we can sell after 12 months (subject to penalty), we also have the ability to hold a little longer to see what rates are announced next. Since there are purchase constraints, the decision to sell is best made after seeing what you'd be offered in the next 6 months — i.e., month 13 of the holding period — rather than relying on the month 7-12 rate earned.

Conclusion

Forecasting CPI-U for a particular date is challenging, but should become easier as the gap between today and that date narrows. A decision to purchase Series I Bonds far away from the next 6-month announcement increases the variability in the annualized rate, but the alternative is to hold off until just before the announcement — and doing so carries an opportunity cost. If the current 6-month rate is sufficiently attractive, it is suggested that we purchase the bonds, but with awareness that we may reverse course if CPI-U declines and rates become unattractive.

For a generic "buy" decision, this assumes the individual has exhausted any high-cost debt options, has sufficient liquidity, and isn't likely to be forced into selling for cash-flow purposes. It's hard to call anything an absolute yes or no without knowing the underlying circumstances.