Estate planning is the process of defining what happens with financial and non-financial matters when you're unable to act — both at death and during incapacity. Think of it as a safety net: build a robust plan, but use it as sparingly as possible. The ideal estate is one where you've already addressed everything during life.

You may find this framing unusual, but it's not to say you should be broke at death — rather that you gave everything away a moment before, rather than a moment after. The former is governed by the rules of gift tax; the latter by estate tax. As we'll see, these are intertwined.

How does estate planning apply to me?

Estate planning is a broad subject and a cyclical process. With changes to federal estate tax law over the past decade, many people think estate planning is no longer necessary. In some cases that's true. The challenge is knowing when you need to plan and when you don't — and a massive part of this is the divergence between federal and state approaches to estate tax. Most searchable articles focus on federal rather than state issues, leaving people with answers that don't consider the impact of their state of residence.

Although many professionals might not want to admit it, there are times where you don't really need an estate plan. If you're young, have no dependents and little in assets, you might not need even a basic Last Will and Testament.

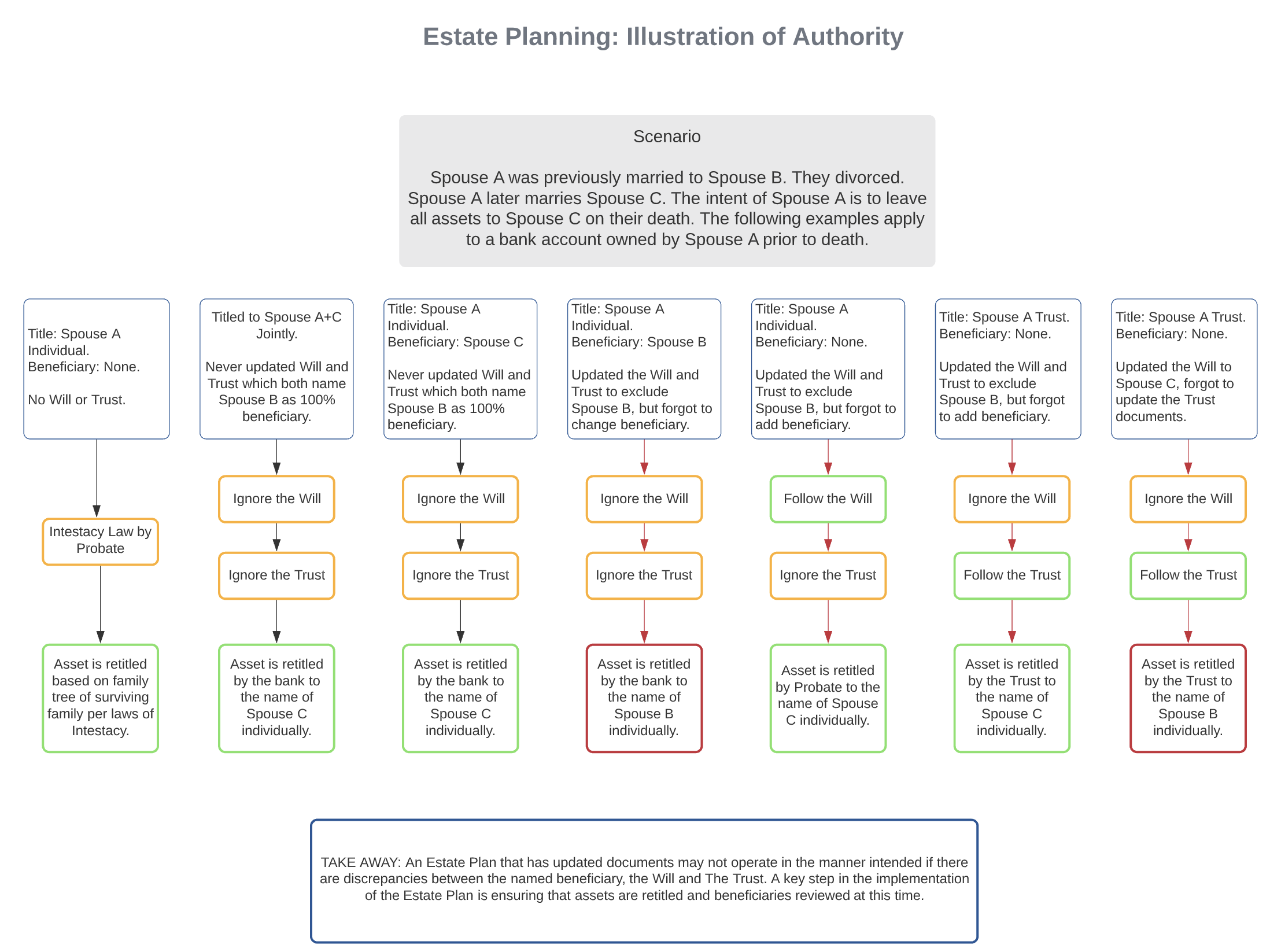

The reason stems from the notion of Rule of Law versus Rule of Contract. A classic example: a person remarries. They have an old Will that very clearly states "leave everything to my spouse" — referring to a prior spouse. That ex-spouse might try to claim rights on a bank account but would fail if the account had been titled with a beneficiary designation. The Rule of Contract outweighs the Will, despite the Will being a legal document. Sometimes this works to your benefit; sometimes it backfires.

Estate planning is more than tax

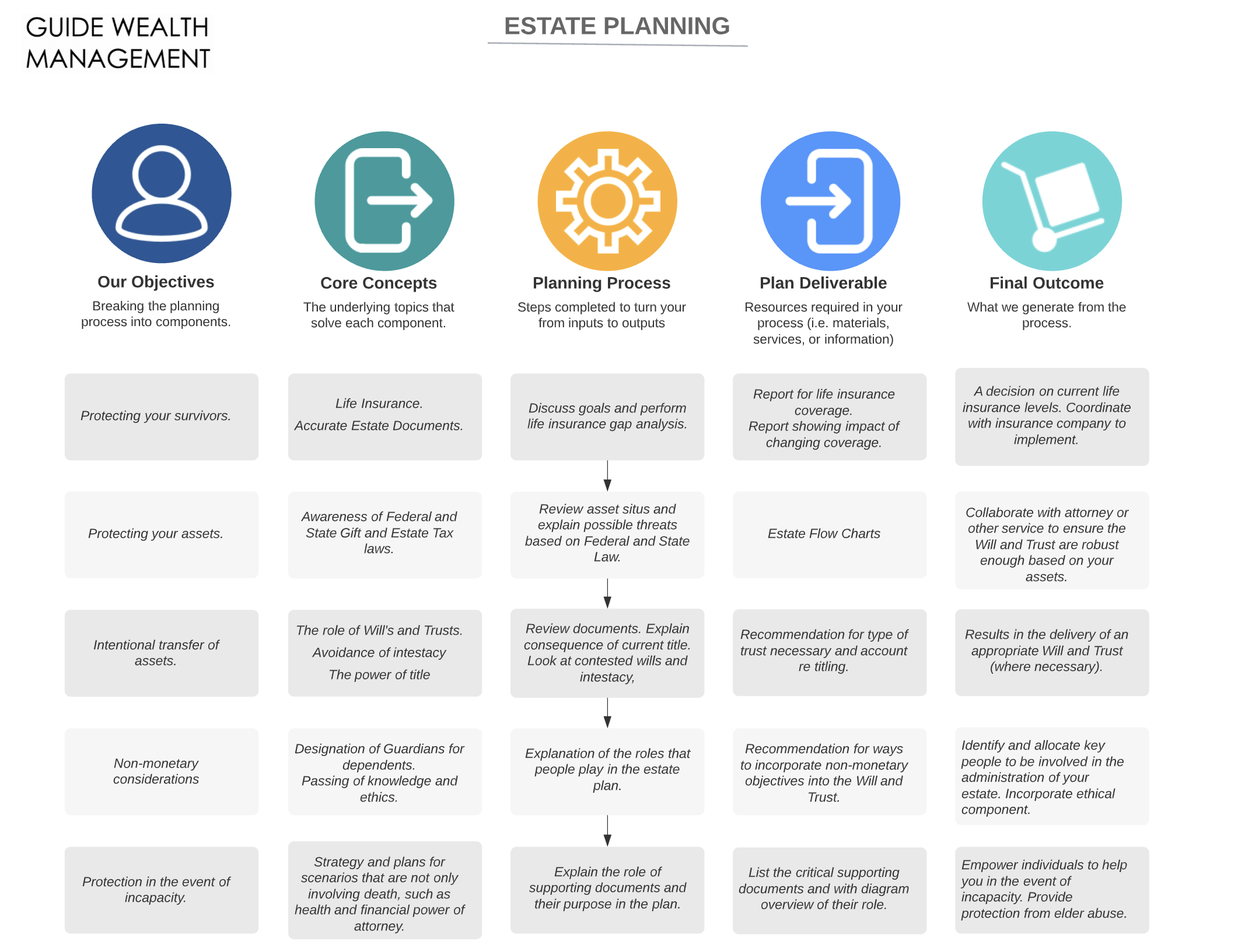

While federal estate tax is less of a concern for many, it's only a small piece of estate planning. In broader financial planning, the estate plan is a pillar — the CFP® Board weights it as 12% of the curriculum, with topics including:

- Characteristics and consequences of property titling

- Strategies to transfer property

- Estate planning documents

- Gift and estate tax compliance and calculation

- Sources for estate liquidity

- Types, features and taxation of trusts

- Marital deduction

- Intra-family and other business transfer techniques

- Postmortem estate planning techniques

- Estate planning for non-traditional relationships

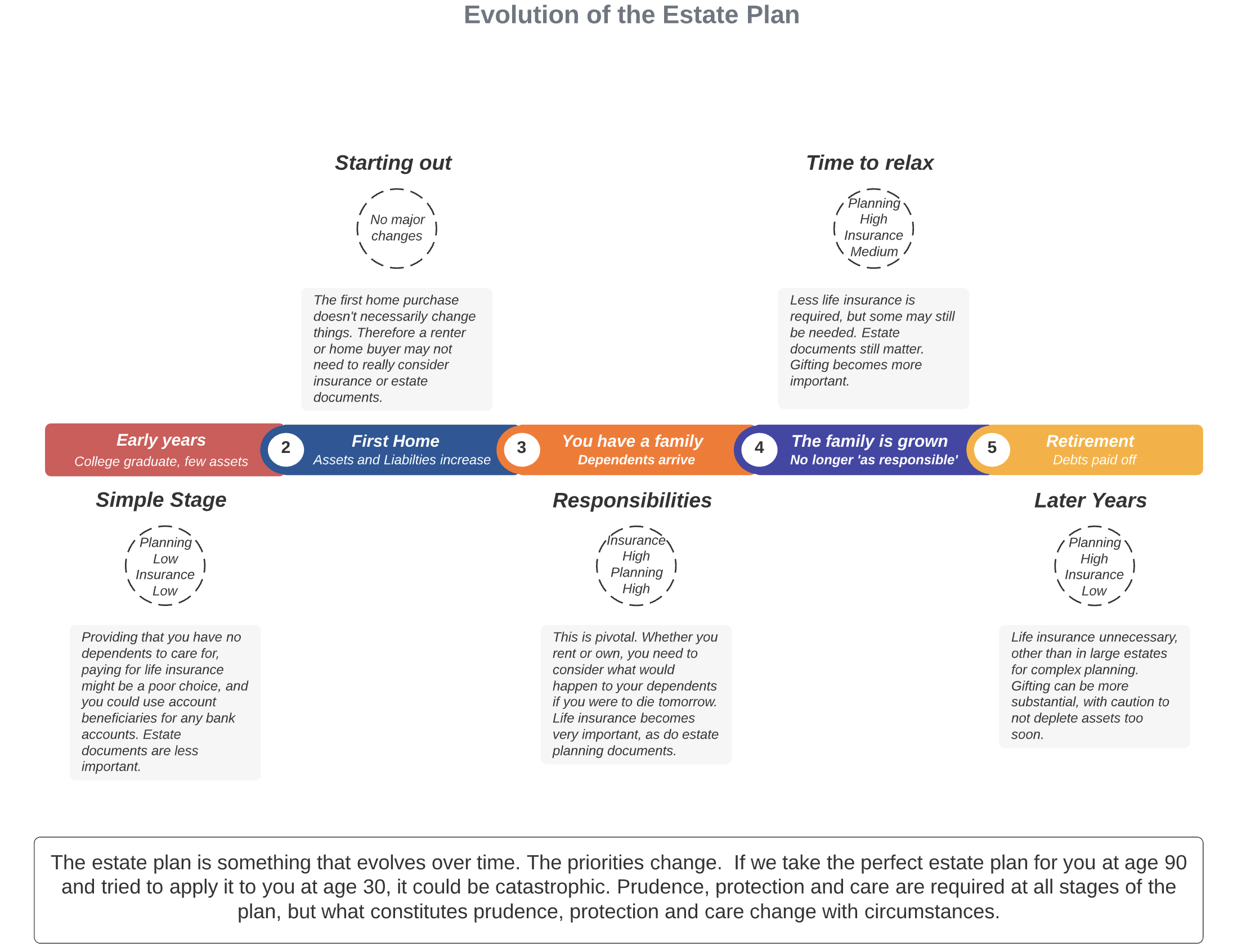

There are many facets here, and they integrate with other elements of financial planning — insurance, gifting — and, perhaps more importantly, the non-financial elements like naming guardians for surviving dependents. Where you are in life and what responsibilities you have will alter the importance of an estate plan, and the components of the plan specifically.

For example, there's a good argument that you only need term life insurance in the "middle years": when you're young with no dependents it's unnecessary, and when you're old you can self-insure via other assets. But it's very common for people to start a family and buy a home using a mortgage, and term life insurance during these years can be life-changing.

Instructions of last resort

If we look at the financial elements of an estate plan — asset titling and transfers, trusts, taxation — we can see that an estate plan is really just taking care of things we failed to do when living. It's the instruction of last resort. If we were to take a perfect financial life, a person would spend their last dollar, laugh at the life they've lived, and then die. There would be no need for a Will, no assets to transfer, no Trusts to form. This doesn't mean they haven't saved and provided for loved ones — it simply means asset transfers are completed during life rather than after.

Think of gift tax and estate tax as the same

While there are some nuances between the two, they are intrinsically linked:

- Gift tax = tax paid on gifts in excess of the lifetime exemption that occur while living.

- Estate tax = tax paid on transfers in excess of that same lifetime exemption that occur after death.

(You may also exclude an annual amount per person from gift tax.)

Further proof: the exemptions are the same. If you used $10M of gift tax exemption during your lifetime, your estate tax exemption is lowered by that amount. If we treat this as one big gift-estate combo for planning purposes, things become a lot clearer.

Behavioral issues

A very common theme: young parents have a financial goal to pay for college so their children can be unburdened by student loans. Frequently, 529 plans are used and a gift occurs from parent to child. There's a method where accounts can be "superfunded" by bunching five years of annual gift exclusions into one — even doubled via gift splitting.

In many cases this is fine. An immediate benefit is insulating the funds from annual taxation, allowing tax-free growth (if used on qualified education expenses). But in some cases it's a bad strategy. The obvious problem: by transferring funds into the 529, they're no longer available for other uses. While there might be annual tax savings on the growth, what about the opportunity cost?

It's a sincere, kind gesture — the parent doesn't want their child paying interest on student loans. But they have a mortgage they're paying interest on, and they can't pay it off because resources are allocated to the 529. Or, in another scenario, an additional $150,000 could cover two years of retirement spending, and use those $0 income years for Roth conversions.

When we bundle this gift-estate-combo together, we're really asking better questions:

- Which strategy teaches the best skills of managing money?

- Which strategy results in the greatest amount of net worth?

A strong argument could be made that a student who graduates with no debt due to a parent's support may not possess the skills to manage a budget. If a parent intentionally decided not to fund college, they might teach prudence and budgeting while building greater wealth to transfer.

Match transfers to your life phases, not theirs

Paying for college is one idea. A better one might be looking at gifts at key stages in your own life. If college years coincide with a time where you still have other debt to manage, depleting yourself of resources requires accepting additional burden — perhaps holding more life insurance because you've overextended. Contrastingly, if you pay for college after the mortgage is paid off, you have a consistent platform to work from. For those who have children later in life, college may coincide with retirement years, in which case it's better to "make them wait" until required minimum distributions are occurring and you have excess annual income to deploy.

You want to give it all away

Ultimately, you want to give it all away — but the timing matters. This is the essence of the estate plan: it's a backup plan for the things you couldn't complete in time.

We want to create the most robust plan possible, but use it as sparingly as possible.

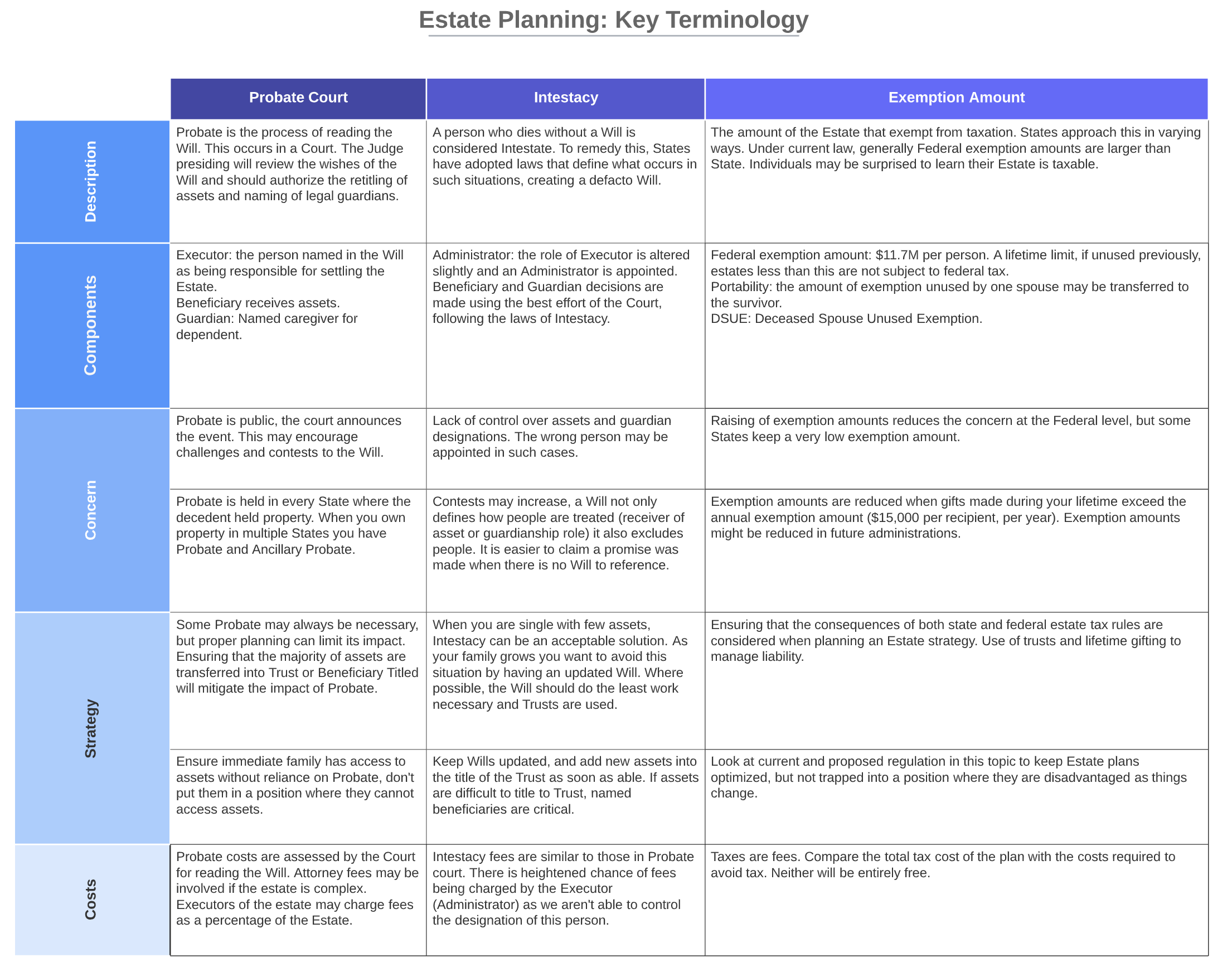

Components of the estate plan

No one size fits all. Everything has a cost — the cost of taxes, or the cost of planning to avoid those taxes. If you have assets just barely exceeding the lifetime exemption, creating an elaborate series of trusts could protect that small excess from taxation but at a cost of many thousands of dollars.

However, that same individual might have many different needs based on the bigger picture:

- If they were married with young children and assets matched with liabilities via a mortgage and other debt, planning might require insurance to help protect dependents in the event of premature death.

- Age alone may be material. A person at 30 with these assets would be expected to live many more years; if spending is less than income, the small excess could quickly grow into something substantial. Trusts are used to freeze the size of the estate.

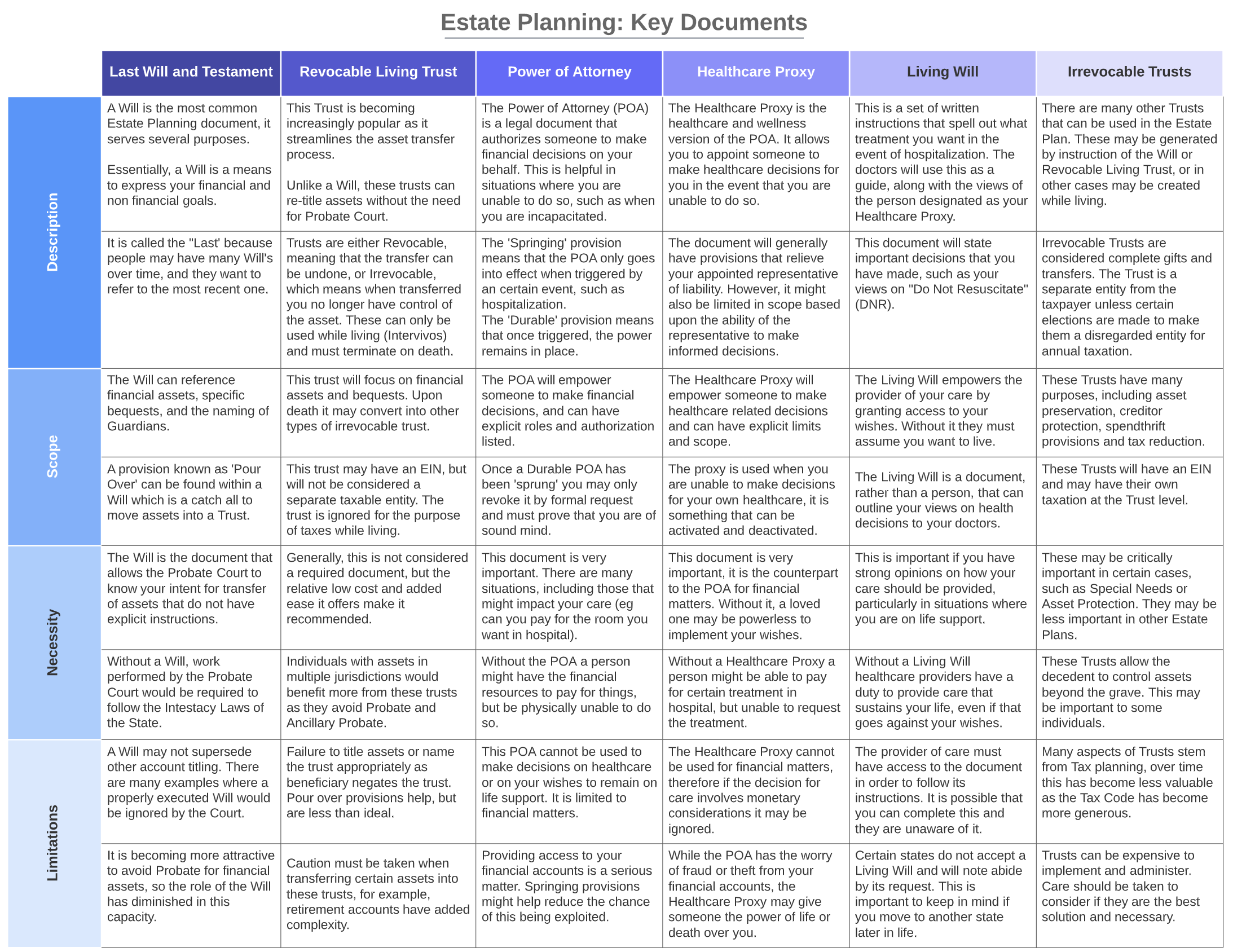

Estate planning key documents

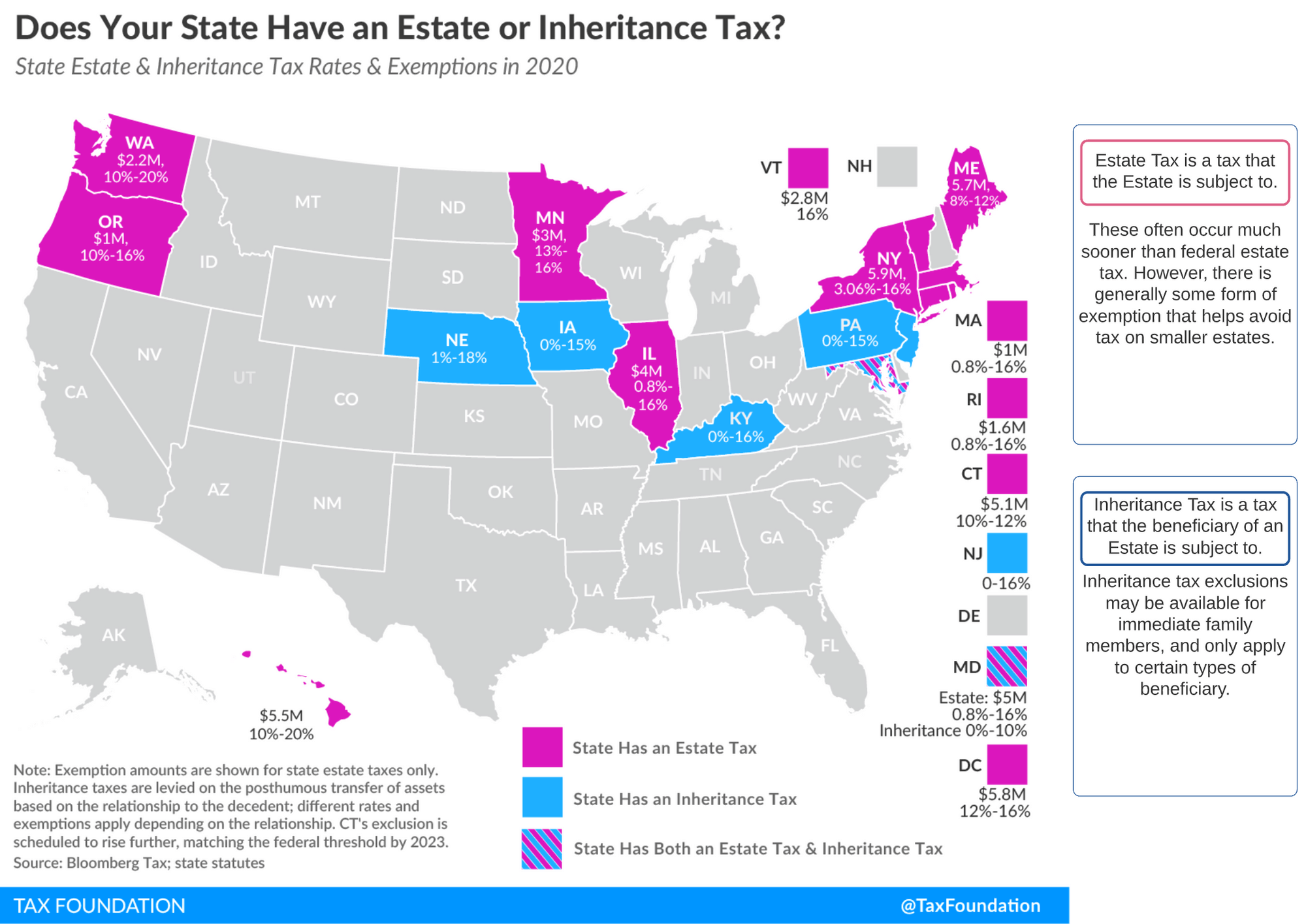

State tax matters

One of the major challenges in any planning process is that each state can implement its own rules regarding estate tax. Some also implement an inheritance tax, applied to certain beneficiaries.

Divergence between state and federal

Two of the most impactful pieces of legislation in estate planning have been Portability (introduced in 2010) and the major increase to the lifetime exemption amount in 2017. However, not all states have implemented Portability, and each state can set its own lifetime exemption — often significantly lower than federal.

Portability is the method of transferring Deceased Spouse Unused Exemption (DSUE) to the surviving spouse. The impact: a married couple electing portability will double the lifetime exemption of a single person, whether they fully use the exemption on the first death or not.

Example without portability

- Spouse 1 dies on January 1st with $7M in assets titled individually, with Spouse 2 receiving 100% via beneficiary designation.

- Spouse 2 dies on February 1st with $14M in assets, leaving everything to a surviving child.

The first transfer occurs at Spouse 1's death — but no estate tax due to the marital deduction (an unlimited amount may transfer between spouses, other than those married to non-resident aliens). The second transfer occurs at Spouse 2's death.

Without portability of DSUE, the excess over a single person's exemption is fully taxable. With the brackets in the estate tax table being compressed relative to income tax, the top rate of 40% arises quickly at $1M and above:

| Amount over exemption (from) | To | Estate tax rate |

|---|---|---|

| $0 | $10,000 | 18% |

| $10,000 | $20,000 | 20% |

| $20,000 | $40,000 | 22% |

| $40,000 | $60,000 | 24% |

| $60,000 | $80,000 | 26% |

| $80,000 | $100,000 | 28% |

| $100,000 | $150,000 | 30% |

| $150,000 | $250,000 | 32% |

| $250,000 | $500,000 | 34% |

| $500,000 | $750,000 | 37% |

| $750,000 | $1,000,000 | 39% |

| $1,000,000 | Above | 40% |

Example with portability

With the same facts, portability allows Spouse 2 to claim the DSUE of Spouse 1, doubling the available exemption. None of the $14M is taxable. Portability can save substantial federal estate tax.

Don't forget the state taxation

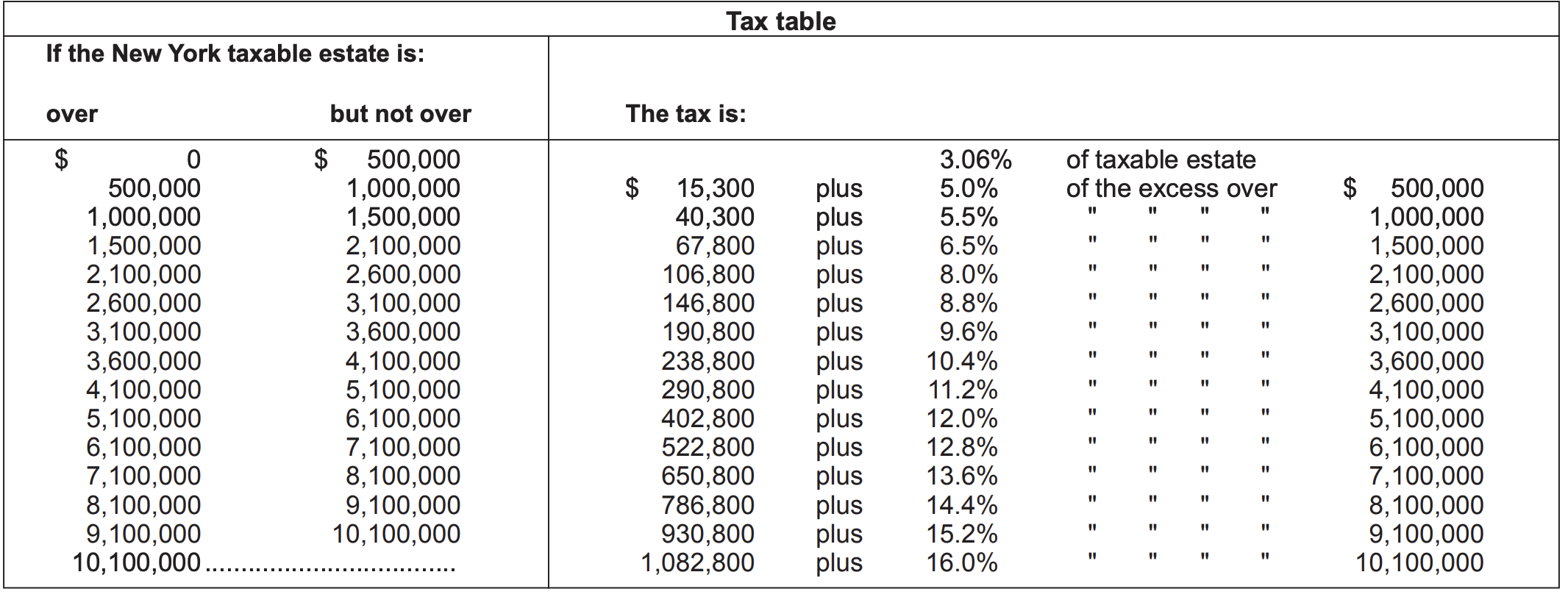

In the example above, we might think portability and the broadened federal exemption would suffice. But we need to keep in mind how the state views the matter. New York is an example where estate tax becomes very burdensome:

- Spouse 1 dies: similar to federal, no tax due to the marital deduction.

- Spouse 2 dies: very different from federal — substantial tax may be due.

Four factors in the New York calculation impact the tax:

- No portability of DSUE (making the $7M from Spouse 1 taxable on the death of Spouse 2).

- A lower lifetime exemption rate.

- A special rule where the exemption is disallowed in estates that exceed 105% of the exemption — referred to as the Estate Tax Cliff.

- Tax rates lower than federal, with a maximum of 16%.

The NY estate cliff

This is a great example of how an individual state may approach estate tax differently. In federal calculation, the lifetime exemption is always allowed, to the extent it hasn't been used during life. In New York, as soon as the estate exceeds the (lower) exemption level by a certain amount, the calculation acts as though the exemption is worth $0.

Due to these divergences, classic estate planning strategies — such as Credit Shelter Trusts — are still in use for estates not subject to federal estate tax. While many think such planning is no longer necessary, this is typically because they're viewing it through the federal-tax lens only.

The use of trusts in the plan

Trusts can be fantastic tools. They are split into two key categories:

- Revocable trusts — disregarded for tax purposes; transfers may be reversed.

- Irrevocable trusts — typically a separate tax entity; transfers cannot be undone. They're moved out of your name and into the name of another entity, though they can still be used for your benefit.

Revocable trusts often contain provisions that create new trusts on death and control the flow of assets to beneficiaries — natural people or other entities. They are attractive because they avoid probate when assets are titled appropriately.

Care needs to be taken with trusts. As noted, with irrevocable trusts you're often at the mercy of the irrevocable nature of the transfer. This can cause issues when a trust has provisions to qualify for certain tax treatment — as we saw with the use of a trust as a beneficiary of a retirement account. Under old law, in order for the trust to qualify it had to allow withdrawals following RMD rules. When the laws governing RMDs changed, these trusts created bottlenecks that could cost the account holder massive amounts of tax penalty.

While trusts can solve complex problems, they can also create new ones, and must be constantly monitored for changes in the underlying tax code.

Get in touch

If you'd like to discuss your own estate plan, feel free to reach out via the contact form.